Today were are going to talk about two advanced types of commercial loans - mezzanine loans and preferred equity. Together they comprise most of the field of structured finance.

Today were are going to talk about two advanced types of commercial loans - mezzanine loans and preferred equity. Together they comprise most of the field of structured finance.

Above I referred to preferred equity as a type of commercial loan. More precisely, preferred equity is NOT a commercial loan, but rather an infusion of fresh equity into an existing limited liability company ("LLC"). The effect, however, is the same.

Example:

John Livingston is a very wealthy real estate investor who owns a huge office tower in New York City. Title to the huge office tower is held in the name of Livingston Ventures, LLC., a single-asset, bankruptcy-remote entity.

A single-asset, bankruptcy-remote entity is usually a LLC that owns nothing else, other than the building. Hence the expression, "single-asset entity". "Bankruptcy-remote" means that title to the property is held in the name of some entity that is NOT John Livingston personally. Mr. Livingston could get drunk someday and plow into a group of 30-year-old surgeons. Their wives could win a $20 million wrongful death action against Mr. Livingston, forcing him into a Chapter 11 bankruptcy, as he rearranged his assets to pay the judgment. The operation of Livingston Ventures, LLC. would be unaffected by such a personal bankruptcy.

Many commercial lenders today therefore require their borrowers hold title to the property in a single-asset, bankruptcy-remote entity. In truth, virtually all sophisticated real estate investors today already hold title to their commercial properties in a single-asset LLC.

Now back to how Mr. Livingston needs cash. He has a $20 million first mortgage on his huge office tower from New York Life at 4.5%. The loan has an enormous prepayment penalty, known as a defeasance prepayment penalty. The first mortgage still has four years until maturity, at which point the borrower can refinance without penalty. Unfortunately Mr. Livingston needs cash now.

The good news is that Mr. Livingston has a ton of equity in his building. The building is worth $35 million, and he only owes $20 million on his first mortgage to New York Life.

He can't apply for a second mortgage for three reasons. First of all, his first mortgage balloons in just four years. The second mortgage lender might have to pay off the $20 million ballon payment in order to protect its $7 million second mortgage.

Secondly, the monthly payments on the $20 million first mortgage are around $80,000 per month. It can often take 18 months to foreclose a mortgage in New York State. Can you imagine making $80,000 payments on the first mortgage for 18 months? Ouch!

Most importantly, however, is that the commercial loan documents on the first mortgage specifically prohibit placing a second mortgage on the property. The moment that a second mortgage is recorded, New York Life can declare it an unauthorized alienation of title (transferring an interest in the property without the lender's permission). They could immediately call their loan and demand to be paid off in full, along with a $3.8 million defeasance prepayment penalty. No way! Yes, way.

Okay, clearly a second mortgage is out of the picture. How about a mezzanine loan? You will recall that a mezzanine loan is not a real estate loan. It's a loan against the membership interests (think of stock) of the LLC (think of a corporation) that owns the property. Because mezzanine loans are personal property loans, not commercial real estate loans, they can be executed upon (foreclosed upon) in a matter of two months. That's a whole lot faster than the 18 months it takes to foreclose a mortgage in New York.

Dave Attell on Breastfeeding:

Ladies, it is amazing how you do that, with a beverage coming out of your nipple, did you know that? Guys, we can't do it. Because if we could, we'd spend the whole time squirting each other.

-------------------

Unfortunately for Mr. Livingston, the commercial loan documents from New York Life specifically prohibit mezzanine loan financing as well. This is true with the commercial loan documents of virtually all life companies, conduits (CMBS lenders), and banks today.

Wait a minute. If mezzanine lenders are prohibited from making their loans after the first mortgage is recorded, when do they ever get to make their mezzanine loans?

Please pay attention here. This is important:

Mezzanine loans must be recorded simultaneously with the big permanent loan in front of it. For example, Citibank might record a $120 million first mortgage, while the Carlyle Group simultaneously records its $35 million mezzanine loan.

Mezzanine loans are large loans. You will seldom close a mezzanine loan of less than $2 million behind a first mortgage of less than at least $8 million. Let me say this again: The first mortgage usually has to be at least $8 million before any mezzanine lender will pay attention to you.

But Mr. Livingston still needs dough. How is he going to tap the huge amount of equity in his building?

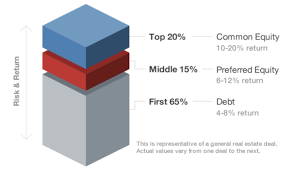

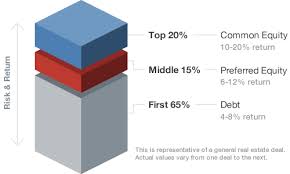

What about preferred equity? As it relates to commercial real estate, preferred equity is an injection of fresh capital (money, dough) into an existing LLC. Preferred equity does NOT have required monthly payments. Instead, the preferred equity only gets paid if the property is generating a surplus of cash flow, but only up to a certain yield; say, 15%.

Now this is important:

If there is a surplus of cash flow, the first member of the LLC to get paid a dime is the preferred equity holder. He's special. Think of the Church Lady from Saturday Night Live. Isn't he special? He is preferred. The other members of the LLC - known as the common members (like common stockholders) - might not get a penny of that surplus cash flow.

The preferred equity holder might not get his full 15% return until the property is sold. For example, there might only be enough surplus income, after paying the first mortgage and any required reserves, to pay the preferred equity holder 8%. The balances of his preferred equity return merely accrues and compounds until the property is refinanced or sold.

What happens if the preferred equity never gets paid at all? If the problem is that the market is crumby, then too bad, so sad; but if the problem is poor management, the preferred equity holder can seize the management of the property.

This brings up an important point. Most commercial loan documents prohibit preferred equity holders from owning more than 49% of the total number of membership interests. We already know that if the LLC sells the property that the first mortgage has the right to call their loan and collect a huge defeasance prepayment. The same is also true if the LLC sell 50% or more of their membership interests. The reason for this is that the lender wants to be able to rely on the experience of his particular borrower. The preferred equity "lender" is unknown to him.

How about the cost of a mezzanine loan versus the cost of preferred equity? The all-in cost of a mezzanine loan today, including the interest rate, the points, and any exit fee, is typically between 8% to 11% today. The all-in cost of preferred equity, including the preferred return, any points, and any exit fee is typically between 12% to 15% today. Mezzanine loans are 2% to 4% cheaper than preferred equity. Just remember, mezzanine loans have to be recorded simultaneously with the first mortgage.

One final point. There are preferred equity providers who will "loan" as little as $750,000.

I have a real treat for you today. A buddy of mine, Yoni Miller of

I have a real treat for you today. A buddy of mine, Yoni Miller of

QuickLiquidity is a direct lender and preferred equity investor providing equity recapitalizations, subordinated debt and partner buyouts on commercial real estate nationwide. QuickLiquidity allows real estate owners to monetize their existing equity while maintaining majority ownership and control of their property without disturbing their existing first mortgage or triggering any prepayment penalties. For more information you can visit www.quickliquidity.com/recapitalizations.html or call Yoni Miller 561-221-0881.

QuickLiquidity is a direct lender and preferred equity investor providing equity recapitalizations, subordinated debt and partner buyouts on commercial real estate nationwide. QuickLiquidity allows real estate owners to monetize their existing equity while maintaining majority ownership and control of their property without disturbing their existing first mortgage or triggering any prepayment penalties. For more information you can visit www.quickliquidity.com/recapitalizations.html or call Yoni Miller 561-221-0881. If you are a conventional buyer of commercial real estate, or if you are a commercial broker, this article is VERY important to you. The reason is because you are about to discover a BIG problem with your next commercial real estate loan.

If you are a conventional buyer of commercial real estate, or if you are a commercial broker, this article is VERY important to you. The reason is because you are about to discover a BIG problem with your next commercial real estate loan.