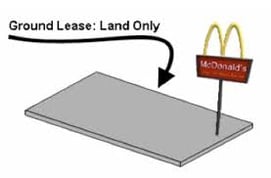

What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.

What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.

Land leases can have any term, but two common lease terms are 49 years and 99 years. Land leases are also called ground leases.

Example: Once upon a time, 60-year-old Tom Grumpy owned a wonderul, three-acre parcel located on the corner of Premier Boulevard and Affluent Way. Every day 5,000 luxury sedans and SUV's drove by this corner. Every developer in town wanted to buy this land and develop a high-end strip center, with shops like Gucci and Prada. Old man Grumpy rejected every offer. "The property is not for sale. I am saving it for my grandchildren."

Enter Susie Raptor, a clever girl. She approaches Tom Grumpy and proposes the following: "Tom, I agree with you. You should not sell this incredible piece of land. It is only going to increase in value over time. Instead, you should lease it to me for 99 years at $10,000 per month. You can use the cash flow to supplement your retirement income, help out your kids, and to pay for college for your grandkids." Tom agrees. Once Happy Tom signs the lease, Susie brings in her architect and her engineer to draw up plans. Eventually Miss Raptor (she drives a lizard-green convertible) brings the project to a local bank, who finances the construction of a gorgeous retail center.

When the construction loan matures, Susie obtains a $12 million takeout loan from a conduit. You will recall that a takeout loan is just a garden-variety permanent loan that pays off a construction loan. When the conduit underwrites the takeout loan, it treats the land lease payment as just one more required operating expense.

When a commercial lender underwrites a commercial loan against the land lessee's interest in a commercial property sitting on leased ground, the lender will insist on an amortization schedule that full-amortizes the loan over a term 10 years shorter than the remaining term of the ground lease. Huh?

Example: Let's suppose that a convenience store sits on leased ground, and the land lease expires in 32 years. Now ordinarily a bank will amortize its loan over 25 years. However, ten years earlier than the 32 years remaining on the land lease is just 22 years. Therefore the bank will amortize its loan over just 22 years.

Example: Let's suppose that a 99-year land lease was written 45 years ago. There is now 54 years remaining on the land lease. Fifty-four years less ten years equals 44 years. Does this mean that some bank will amortize its permanent loan over a whopping 44 years? Yes? Yes? Nice try. Ha-ha! The longest amortization schedule that most banks will ever use is 25 years for a commercial building. Unfortunately this building was constructed 54 years ago. This is an old-old building. Because of the age of the building (its wearing out), the bank will probably insist on an amortization schedule of just 20 years.

"Hey, George, what happens to the $7 million building on the land when the ground lease expires?" Answer: It reverts back to the land lessor. The land lessor is the guy who owns the land now and whose father or grandfather (usually) originally leased out the land.

"But George, what if the apartment building adjoins Central Park in New York City? What if the building is worth $100 million. At the expiration of the ground lease, both the land and the building still reverts back to the land lessor.

Can the land owner get a loan against his leased fee interest? A leased fee interest is ownership of land (and building) that is leased out to someone else. To answer the question about whether the land lessor can get a commercial loan, the answer is yes, in about a nanosecond. In real life we don't see many of these commercial loan requests. The families that own the land underneath huge commercial buildings are typically richer than Crassus (often because their grandfather refused to sell the land).

Is it possible to get a land lease longer than 99 years. The answer is no. If a party leases land for longer than 99 years; say, 110 years; the land lessor is deemed to have sold the property to the land lessee. It is against public policy to have real estate tied up for too many generations.

Obviously a perfect ground-lease deal is one with a very long remaining term and with a very small land lease payment.

Do you need a commercial loan against a property sitting on leased land? This is an ideal time to use C-Loans.com. Enter your commercial loan as if it was a garden variety first mortgage request; however, in the Special Issues section, be sure to write, "The subject property sits on leased ground. The remaining term of the land lease is 48 years, and the monthly land lease payments are $5,820 per month."

Want to finally learn commercial real estate finance? You can succeed as a financier with just a high school education, if (1) you have a pleasant, sales-type personaility, and (2) your English skills are excellent; and (3) you learn your material thoroughly. Remember, when you are selling commercial mortgage financing, you are working with the wealthiest, most upper-crusty class of investors. You can't fake it.

My courses are dirt cheap. Buy them. Inhale them. I was thrilled to receive the following testimonial this month:

"I don’t know if you remember me but about 6 months ago I sent you a Thank You for selling me your VHS tape course back in 2003 when I first got into lending business. You and I both had no grey hair back then. Here we are 15 years later and I am one of the most successful commercial, out of the box, hard money lenders in South Florida. You didn’t know it but I watched your VHS tape at least 10 times (obviously now DVD's) and you were my mentor back then. I still use your broker agreement." -- Ron Holy mackerel, Ron. Thanks!

Be sure to note that Ron is now a successful hard money lender, not just a broker! Those of you with brains will - sooner or later - finally grasp the secret of commercial mortgage finance: It's the loan servicing income, silly. My own hard money shop's servicing portfolio just passed $50 million this month. That's s coool $1 million per year in loan servcing income - $ 83,333 per month, every month, whether we close a new loan that month or not.

Servicing loans? I can't service loans, why... why... I'm left-handed! Quit being a weenie. My lovely bride and I serviced our first 20 loans or so, out of our house, using payment books. Heck, if you want, you can hire a sub-servicing company to service your performing deals for around $10 per $30 per month. The idea is to charge $600 per month for servicing a hard money loan and then service it at a cost of just $30 per month. Comprende?

The best deal is to buy both programs at the same time for just $849, plus ($30?) shipping and handling.

Do you need a purchase money lender who will actually go to 75% loan-to-value? Do you need a lender who will allow the seller to carry back a second mortgage? Does your client have a balloon payment coming due on his commercial property? Has your bank offered him a discounted pay-off? Does your borrower have less-than-stellar credit? Is your client's company losing money? Is your borrower a foreign national? Do you need a non-recourse loan? Do you need a commercial loan with no prepayment penalty? Is your client's commercial property partially vacant? Do all of your commercial leases run out in the next 18 months? Do you need a lender who will allow a negative cash flow? Do you need a lender who will also look at the borrower's global income - income from salaries, other investments, etc.?

Our hot, new product is a blanket loan against a portfolio of rental homes. Rental homes? Yup, as long as there are at least five homes or units, we consider this to be a commercial loan. We even offer a partial release clause. This loan is ideal for speculators.

Get free training in commercial real estate finance. I try to blog twice a week, and its always training. I use these articles to train my sons (and hopefully soon my daughter).

Got a buddy or co-worker who would benefit from free training in commercial real estate finance.