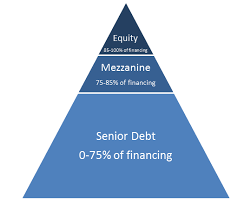

The Crittenden Real Estate Finance Conference is one of the most prestigious conferences in the entire commercial real estate finance industry. Folks, these are the Big Boys. They talk casually about deals with capital stacks (a first mortgage plus a mezzanine loan plus preferred equity plus joint venture equity plus the developer's equity contribution) as large as $100 million. My son, Tom Blackburne, and I attended this conference last week. Here are his observations:

May 8, 2017

I recently attended a Crittenden Conference in Costa Mesa, CA, where all the big-wigs (Citi, Wells Fargo, Blackstone, etc.) spoke about the state of the current market and gave their projections on the future. To no surprise, just about every panel that spoke discussed what opportunities they are seeing in the marketplace. Retail is on the out, because the "Amazon Effect" is well underway. There is no longer a high need for retail space when e-commerce is dominating the industry. Even companies like Wal-mart are now shipping groceries to your doorstep. As a result, the shipping (trucks, boats, planes, etc.) industry is hot and projected to increase in the foreseeable future.

My dad asked the panel about a new term they were frequently using - Last Mile Retail.

Last Mile Retail is the latest topic buzzing through discussions of industrial real estate. It refers to the final stage of online purchasing and the travel of goods to the buyer from a distribution center. The obvious benefit is short lead-time delivery options for retailers/wholesalers to transport products to consumers at their place of business or residence.

Industrial is also hot. Opportunistic lenders and investors should really be considering multi-tenant industrial properties in primary and secondary markets, especially in gateway and 24-hour cities. C-Loans is also looking to capitalize on the opportunities presented in the current marketplace by adding lots of these new private bridge/construction lenders, unregulated family offices, etc. to our portal!

At the conference, there was an overarching sense of optimism, despite the obvious uncertainty of what to expect. The Trump factor, I thought, would be a big topic and area of concern, but I was wrong. Everyone who spoke, shared the same opinion: Trump's regime will only have a marginal affect on the real estate market as a whole. Trump plans to look at the current regulations affecting the banks and other regulated lenders, but even if he makes some changes, the Regulators (the companies doing the actual auditing) will be very slow in changing their practices and mentalities.

On this point, the most highly discussed topic was Construction Lending. It is incredibly difficult to get conventional construction financing right now, because of the HVCRE requirement. This is a term you need to remember: High Volatility Commercial Real Estate. HVCRE has put restrictive stipulations on what is considered equity, amongst many other restrictions, in response to the Great Recession. One-third of all community banks that failed in the last downturn were due to bad A&D lending practices. There are 2,500 fewer banks now than in 2008. Who is capitalizing on this gap in the marketplace? Private, unregulated construction lenders. Can anyone guess how many new small banks were formed in 2016? Just one.

The other major topic of the conference was the dichotomy of the mortgage broker's mind set. What I mean here is that a broker working a lead has two factors driving him one direction or the other: Certainty of Closing or Easiness/Speed of Processing. Good brokers will look at a deal and instantly know which direction to take. Some guys default to the lenders who move the quickest. While other guys stay loyal and bring deals to their lenders that they know close loans. This is where Blackburne & Sons, our sister company, makes its name.

Blackburne & Sons has never been the quickest, but you bet damn sure they close loans. They were one of the few small-balance hard money lenders actually closing loans during the Great Recession. In large part to the leadership and wise underwriting of Angelica Gardner, the EVP, and the unrelenting nature of Alicia Gandy, the longest tenured employee and hardest working loan officer in the company.

Private-money lenders like Blackburne & Sons are not competing with community banks anymore. They are competing with unregulated private bridge lenders that close loans quickly. Many of which, can be describe as non-prime, wall street lenders. Please read my father's blog for more information on this type of lender, which you can find here. Blackburne & Sons has been in business for 37 years and will remain in business for a very long time, because of the concept of Certainty of Closing.

My final note on the Crittenden Conference: If you know my father, George Blackburne, and have read any of his work, then you will know the number 1 lesson in all CREF is that, "Bankers make loans to their friends." What he means here is that banking is relationship-driven. Banks only want to lend money to repeat customers, people whom they have a previous relationship with. Remember this concept before asking Wells Fargo for a new construction loan.

On a different note, I want to take this time to publicly thank Michael (Mick) Carlson for his years of managing C-Loans effectively. Mick has now moved on to bigger and better things, and we genuinely appreciate his service and wish him the best of luck. Going forward, I, Tom Blackburne, will be your point of contact for all things C-Loans. Please reach out to me for any help with your lending parameters, questions, or even for a simple introduction. I appreciate your time and hopefully together, we can collectively make C-Loans more profitable this year, and in turn have more loans for you to close!

Sincerely,

C-LOANS, INC.

Thomas H. Blackburne

General Manager

(574) 210-6686 Best

(916) 338-2328

tommy@blackburne.com

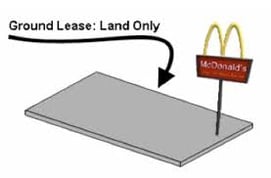

What is a land lease? A

What is a land lease? A

How can you tell if a commercial construction loan request is dead on arrival?

How can you tell if a commercial construction loan request is dead on arrival?

This training article will teach you the difference between a commercial bank and an investment bank. We will also discuss merchant banks.

This training article will teach you the difference between a commercial bank and an investment bank. We will also discuss merchant banks.

"Don't sell the steak, sell the s

"Don't sell the steak, sell the s

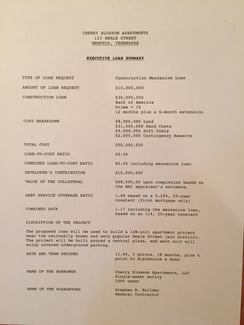

This article should help both complete newbies and near-experts in commercial mortgage finance. I will teach you newbies how to prepare a basic commercial loan Executive Loan Summary. I will teach you old pro's how to lay out an Executive Loan Summary for a construction

This article should help both complete newbies and near-experts in commercial mortgage finance. I will teach you newbies how to prepare a basic commercial loan Executive Loan Summary. I will teach you old pro's how to lay out an Executive Loan Summary for a construction

Long before a mezzanine lender or equity provider will issue a term sheet, the sponsor first has to attract the lender's interest. By the way, the

Long before a mezzanine lender or equity provider will issue a term sheet, the sponsor first has to attract the lender's interest. By the way, the

I have been requested to help raise about $5.5 million in venture equity for a multifamily development project. This endeavor will give us a good example of structured finance.

I have been requested to help raise about $5.5 million in venture equity for a multifamily development project. This endeavor will give us a good example of structured finance.

A reader asked George a commercial loan question, "Do you have access to commercial lenders who do not require income verification?"

A reader asked George a commercial loan question, "Do you have access to commercial lenders who do not require income verification?"

Lets suppose you're working on a commercial loan, and the lender has used a term with which you are unfamiliar or confused. You can now ask me a question about commercial real estate finance, and I'll try to answer it that same night in a blog article.

Lets suppose you're working on a commercial loan, and the lender has used a term with which you are unfamiliar or confused. You can now ask me a question about commercial real estate finance, and I'll try to answer it that same night in a blog article.