Cute Halloween joke:

Cute Halloween joke:

Mr. and Mrs. Hill, along with their three children, were on a touring holiday in Transylvania, where they stopped for the night in Count Dracula's castle. During the night, the evil Count sucked the blood out of all of them and put them in coffins in his vaults. The next night, Dracula sat by the organ thundering out loud music, while down in the cellar the poor Hills stirred in their coffins. They made their way up to the organ gallery, and when Dracula saw them, he said, "Welcome to the Vampire Club. The next tune is especially for you." And guess song he began to play? "The Hills Are Alive to the Sound of Music."

Are referral fees legal on commercial loans?

Absolutely, yes! Final answer. Remember, I am an attorney, and my private money commercial mortgage company - Blackburne & Sons - has happily been paying referral fees on commercial loans for almost forty years.

Don't I have to be licensed?

Only nine states that I know of - California, Arizona, Arkansas, Florida, Maryland, Nevada, North Dakota, South Dakota and Wisconsin - even require a license to broker commercial loans. (Careful. There may be one or two more.)

Therefore, most states have no licensing requirement whatsoever to broker commercial loans. The state licensing scheme might read something like, "A license is required to broker mortgage loans." This language makes it seem like a license is required to broker commercial loans... until you look up the definition of "mortgage loan". A mortgage loan is defined as a loan on a one-to-four family dwelling.

But even in states that require a license to broker commercial loans, referral fees are perfectly legal, as long as you do not negotiate loan terms or try to fetch documents.

Therefore, in states requiring a license to broker commercial loans, you must never talk to the borrower about interest rates, points, the term of the loan, or the prepayment penalty. In those nine states, you must not collect tax returns or financial statements for the lender.

But as long as you work on a name and number referral basis only, then you are perfectly legal in EVERY state.

How large is the typical referral fee on a commercial loan?

C-Loans.com once paid a referral fee of $21,250. Wow. The loan amount was $17 million, so a referral fee of this size is pretty rare.

More commonly, the typical referral fee on a commercial loan is around $1,000 to $2,000. That ain't hay for just a name and a phone number.

The most common formula is some percentage of the lender's or mortgage broker's loan fee - usually either 10% or 20%. Blackburne & Sons pays a referral fee on commercial loans of 20% of our net loan fee.

How do I refer commercial loans?

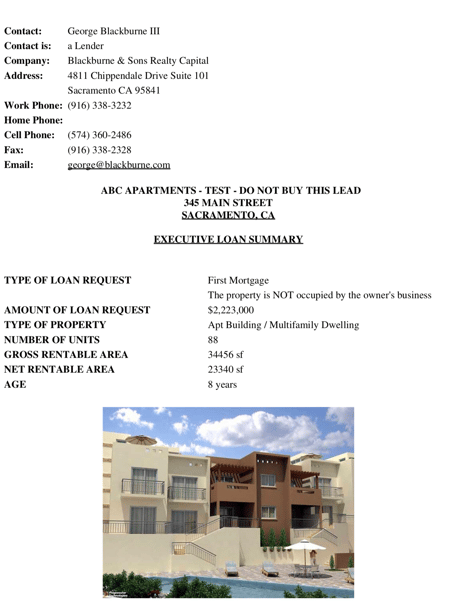

If you know how to recognize a hard money loan, and you want to refer a commercial hard money loan to Blackburne & Sons, please call our office at 916-338-3232 and ask for a loan officer.

You can also email Alicia Gandy or George Blackburne IV (age 35), our loan officers, and deliver the lead this way.

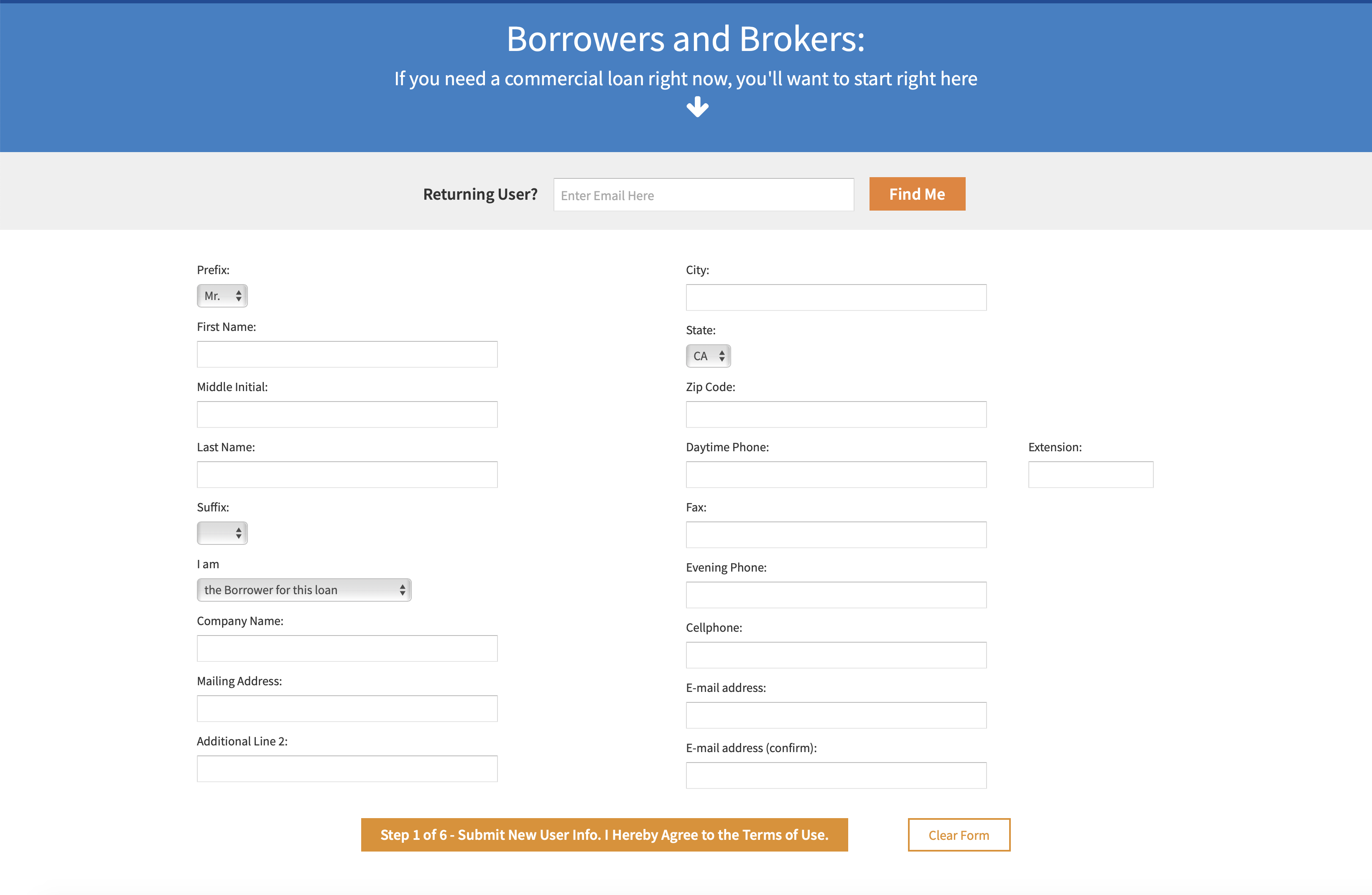

Most of you guys are not experts in commercial real estate finance, however, so you would be wiser to just send your referral leads to me, George III (the old man), by inputting your commercial referral leads here. Be smart. Please bookmark this Referral Leads Input Form right now.

Want to earn huge referral fees in your sleep?

Do you remember that $21,250 referral fee that I mentioned above? We paid that huge fee to a guy named Alan Dunn, and Alan was asleep when he sent that lead to us.

What? Huh? How could he be asleep when he referred that $17 million commercial loan? Alan Dunn created a link on his website entitled, "Commercial Loans", and he pointed that link to C-Loans.com.

C-Loans.com is programmed to capture the URL of the referring site. When this big $17 million loan closed, we looked up the loan application. Automatically printed at the bottom of the loan application was the URL of Alan's website. Imagine Alan's surprise when he got a call, "Hey, Alan. We have a check here for you for $21,250!"

How can I be sure that I won't be cheated?

In truth, you can't be sure, but it may give you a little confidence to know that I am an Eagle Scout, and so are both of my sons. My sons and I also went to Culver Military Academy, where we lived under an Honor System. A cadet does not lie, cheat, or steal.

I am attorney, licensed in California and Indiana. My family hard money mortgage business also services about $45 million in hard money loans for about 900 private investors. The average daily balance in our trust accounts is on the order of $300,000 - and after payoff's, that amount can surge to over $1 million. We have also been servicing hard money commercial loans for our elderly private investors for almost 40 years.

My point is that if we were ever going to become crooks, we probably would have run off with at least $1 million out of our trust accounts thirty years ago. :-) And there was no way that Alan Dunn would have known about his big loan closing, but for our family honor code.

But watch out for the link police.

A referral partner of ours made the mistake of adding too many links to C-Loans.com on his website. The poor guy had his front door kicked in by the FBI at 3:00 in the morning. They dragged him out of bed, beat him batons, and took him away. Despite the frantic pleas of his wife, he was never heard from again. Guantanamo? All because he put too many links to C-Loans.com on his website...

By now you have probably figured out that I am joshing you. Haha! There is no law against putting six or seven links to C-Loans on your website. You can put some links at the top of your pages, some at the bottom, some in the middle, and some in the body of your articles.

The links might say, "Commercial Loans", "Commercial Mortgages", "Commercial Financing", or "Apply for a Commercial Loan." The more links you create, the more chances you have of earning some huge referral fees.

Note: Our referral fee links do NOT work in emails. Please call Tom Blackburne at 574-210-6686 if you have a regular email newsletter. He will create a special kind of link for you.

How large of a referral fee does C-Loans.com pay?

Our hyperlink referral fees are 12.5 basis points. For example, on a $4 million loan, your feral fee would be 0.125% of $4 million - which equates to $5,000.

Important Note: On deals larger than $5MM, closed by banks, credit unions, life companies, and agency lenders, C-Loans itself only earns 25 basis points. Our referral fee is then 8.33 basis points.

So give yourself a chance to make some serious dough in your sleep. Now a confession. We don't know for sure that Alan was actually asleep when his borrower found his Commercial Loans link, but he certainly could have been! Haha.

Were you wise enough to open and bookmark this Referral Leads Input Form?

If you are a well-heeled real estate investor or a commercial real estate broker, you really need to pay attention to today's article. I am going to show you how to use a USDA commercial loan to obtain 90% leverage on a rental property (not just on an owner-occupied property) in an Opportunity Zone. For once, the Federal government is going to help you, even though you had the selfishness to work hard and build wealth.

If you are a well-heeled real estate investor or a commercial real estate broker, you really need to pay attention to today's article. I am going to show you how to use a USDA commercial loan to obtain 90% leverage on a rental property (not just on an owner-occupied property) in an Opportunity Zone. For once, the Federal government is going to help you, even though you had the selfishness to work hard and build wealth.

If the world's money supply starts to contract again, like it did in 2008, commercial real estate investors and those of us in the commercial loan business are going to be painfully affected

If the world's money supply starts to contract again, like it did in 2008, commercial real estate investors and those of us in the commercial loan business are going to be painfully affected

I have an exciting story for you today about the darkest hours of the Great Recession; but first some background.

I have an exciting story for you today about the darkest hours of the Great Recession; but first some background.

You may find this shocking, but

You may find this shocking, but

First, just a quick reminder that C-Loans.com is now giving away free

First, just a quick reminder that C-Loans.com is now giving away free

You should never-ever submit a commercial loan package to a commercial real estate lender without at least one picture of the subject property.

You should never-ever submit a commercial loan package to a commercial real estate lender without at least one picture of the subject property.

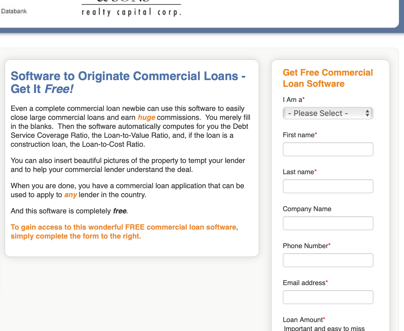

I am often asked, "Where can I get some commercial loan origination software?" This sounds like an intelligent question. After all, there are dozens of vendors who sell similar software for residential mortgage loan originations.

I am often asked, "Where can I get some commercial loan origination software?" This sounds like an intelligent question. After all, there are dozens of vendors who sell similar software for residential mortgage loan originations.

In the past two weeks, North Korea conducted an intermediate range missile test, and then it conducted another test the next day. Trump reassured us that it was no big deal. His agreement with Kim was not to test ballistic missiles, not intermediate range missiles. Then the Russians tested a hypersonic missile, and it was a disaster. More on this later.

In the past two weeks, North Korea conducted an intermediate range missile test, and then it conducted another test the next day. Trump reassured us that it was no big deal. His agreement with Kim was not to test ballistic missiles, not intermediate range missiles. Then the Russians tested a hypersonic missile, and it was a disaster. More on this later.