This training article will teach you the difference between a commercial bank and an investment bank. We will also discuss merchant banks.

This training article will teach you the difference between a commercial bank and an investment bank. We will also discuss merchant banks.

Recently C-Loans.com introduced a pretty cool offer. If you give us the contact information of just one loan officer at a bank making commercial real estate loans, we will give you a free list of 750 commercial lenders. Heck of a deal. But guess what? Some rookie commercial mortgage brokers have been inserting their own names in place of a bank loan officer. Huh?

There are two issues here. First of all, unless you have your own money to lend, and unless you service these loans, you are not a lender. Life companies get money to loan from insurance premiums. Banks, credit union unions, savings banks, and hard money mortgage pools get their dough to lend by accepting deposits. It seems simple, but people often forget that in order to be a lender, you actually need to have money to lend; otherwise, you're just a broker. Secondly, a commercial bank is an institution that accepts deposits and whose deposits are insured against loss by the FDIC. Hellooo? Unless your deposits are insured by the FDIC, you are not a commercial bank.

Okay, so what is an investment bank? Historically an investment bank was an institution that took companies public. In other words, an investment banker, like Barings Brother (established in 1782), sells a company's stock to the public and maintains a market in the stock. Maintaining a market in a stock means matching buyers and sellers, and in a sudden panic (e.g., Napoleon conquers Northern Italy), buying some shares itself to prevent a total rout in the stock price.

Investment banks aso sell bonds for large corporations and various governmental entities, like the Federal government, states, counties and large municipalities. For example, suppose you're CIT Financial (a huge business lender), and you are bullish on the economy. You want to borrow $1 billion from the public at, say, 3%, and lend it out to middle market companies at 7.5%. By the way, a middle market company is a firm with annual revenues of between $50 million and $1 billion. CIT Financial might retain Morgan Stanley, an investment bank, to issue and sell its bonds.

Examples of investment banks include Goldman Sachs, Morgan Stanley, Barings Brothers (bankrupt and dissolved), Lehman Brothers (bankrupt and dissolved), Credit Suisse, Merrill Lynch (now owned by Bank of America), Deutsche Bank, and Nomura. In its simplest terms, you can think of an investment bank as a stock broker.

Okay, then what is a commercial bank? First of all, the word "commercial" merely means "business". The garden-variety banks that you see on the main thoroughfare going through your town are called commercial banks, to distinguish them from investment banks and merchant banks. A commercial bank is a company that accepts deposits and uses those deposits to make loans to companies and consumers. These deposits can take the form of a checking account, a savings account, or a certificate of deposit (C.D.). These deposits and C.D.'s, up to $250,000 per depositor, are insured against loss by the Federal Deposit Insurance (FDIC).

The name of every commercial bank contains the word, "Bank", 99% of the time at the end of the their name; e.g., Oak Bank or Granite Bank. It is highly illegal for any other type of company to include the word, "Bank" or "Bancshares", anywhere in their name. A lot of commercial mortgage brokers make this mistake, and they end up getting hit with a serious fine.

Now what is a merchant bank? A merchant bank is a financial institution that provides capital to companies in the form of share ownership instead of loans. The reason why a merchant bank wants to buys shares instead of making loans is because the types of deals that a merchant bank invests in are incredibly risky. For example, in the late 1700's and early 1800's, a merchant bank might provide 100% of the cost to finance a trading ship to take British goods to India and trade them for Indian gold, Chinese silks, etc. The merchant bank might expect to make 500% on its investment. Modernly a mechant bank might invest in a late-stage round of venture capital funding.

But here's the truth of it: There are very few, honest-to-goodness, merchant bankers. I would not fall off my chair if there were fewer than 200 legitimate merchant bankers in the entire country. If you ever meet a guy at a mortgage conference, and he claims to be a merchant banker, there is a 90% chance that he is either a big blowhard (who has no clue what a real merchant bank is) or he is an outright con man. If you ever meet a "lender" boasting that he is a merchant banker, there is a 99% chance that he is an advance fee scammer. I once wrote an excellent article on how to spot advance fee scammers.

You need a commercial real estate loan, and you have diligently been doing your research. Is it finally time to actually apply for that commercial loan?

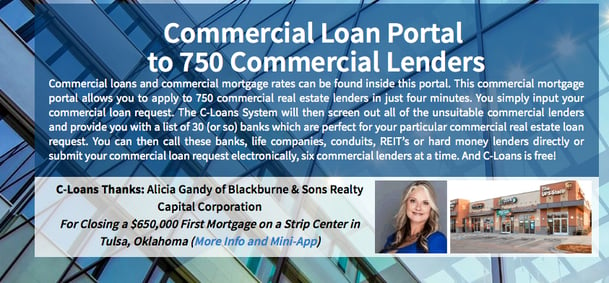

For just $79.95 you can buy a recently updated list of over 2,500 commercial lenders. If money is tight, you can buy a Regional List (750+), for the region that contains the property in question, for just $39.95.

Many commercial mortgage brokers are excellent salesmen, but they starve because they make a dozen preventable mistakes every single day. This 5-hour course in the Practice of Commercial Mortgage Brokerage contains more than 60 practical lessons in commercial mortgage brokerage. I consider it to be the crown jewel in my training series, the best of my life's work. It is the only course I sell that comes with a 100% satisfaction gurantee.

Do you need a business loan secured by accounts receivable, inventory, or equipment. Do you need a lease to aquire some piece of equipment?

We have a superb multifamily program with "A" quality rates for deals with a tiny black hair on them.

Blackburne & Sons, my own hard money shop, offers bridge loans for just 1 point.

Every commercial mortgage broker should use a fee agreement on every commercial loan. Our agreement is quite short, and it is fair to both the borrower and the mortgage broker. You commercial mortgage brokers will kick yourself when you lose a $20,000 fee.

Do you own a real estate or mortgage website? By simply putting a "Commercial Loans" link to C-Loans.com on your web site, your web site can work day and night to generate referral fee income. We once paid $21,250 to a guy named Alan Dunn. Somebody came to his website, saw a "Commercial Financing" link, clicked on it, came to C-Loans.com, and then applied for $17 million loan. Alan was asleep at the time! (We actually have no way of knowing that, but Alan certainly could have been asleep, and it makes for a great story. Ha-ha!)

Have you tried our latest commercial mortgage portal? CommercialMortgage.com has four times more lenders than C-Loans.com, and it is far easier to enter a deal.

Is it finally time to actually learn the profession that you practice? Just sayin'...

Did you learn something today? Get two free training lessons in commercial real estate finance every week.

Got a buddy or a co-worker who would benefit from free training in commercial real estate finance (CREF)?

"Don't sell the steak, sell the s

"Don't sell the steak, sell the s

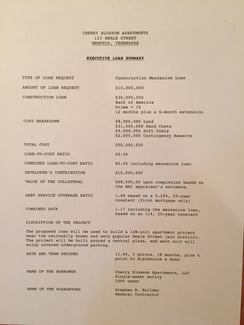

This article should help both complete newbies and near-experts in commercial mortgage finance. I will teach you newbies how to prepare a basic commercial loan Executive Loan Summary. I will teach you old pro's how to lay out an Executive Loan Summary for a construction

This article should help both complete newbies and near-experts in commercial mortgage finance. I will teach you newbies how to prepare a basic commercial loan Executive Loan Summary. I will teach you old pro's how to lay out an Executive Loan Summary for a construction

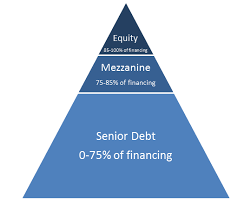

Long before a mezzanine lender or equity provider will issue a term sheet, the sponsor first has to attract the lender's interest. By the way, the

Long before a mezzanine lender or equity provider will issue a term sheet, the sponsor first has to attract the lender's interest. By the way, the

I have been requested to help raise about $5.5 million in venture equity for a multifamily development project. This endeavor will give us a good example of structured finance.

I have been requested to help raise about $5.5 million in venture equity for a multifamily development project. This endeavor will give us a good example of structured finance.

A reader asked George a commercial loan question, "Do you have access to commercial lenders who do not require income verification?"

A reader asked George a commercial loan question, "Do you have access to commercial lenders who do not require income verification?"

Lets suppose you're working on a commercial loan, and the lender has used a term with which you are unfamiliar or confused. You can now ask me a question about commercial real estate finance, and I'll try to answer it that same night in a blog article.

Lets suppose you're working on a commercial loan, and the lender has used a term with which you are unfamiliar or confused. You can now ask me a question about commercial real estate finance, and I'll try to answer it that same night in a blog article.

To understand our new feature, you need to understand tombstones. A

To understand our new feature, you need to understand tombstones. A

TILA and RESPA are Federal laws designed to give borrowers advance disclosure of the costs of the loans for which they are applying. Under the new Dodd-Frank regulations, t

TILA and RESPA are Federal laws designed to give borrowers advance disclosure of the costs of the loans for which they are applying. Under the new Dodd-Frank regulations, t

This is going to be a very short training article because the Chinese were right. A picture is worth a thousand words. Today a mortgage broker submitted the attached picture on his

This is going to be a very short training article because the Chinese were right. A picture is worth a thousand words. Today a mortgage broker submitted the attached picture on his