A purchase money commercial loan is a commercial loan that is used to buy a commercial property and which is secured by the same property. For example, if you refinanced your free-and-clear apartment building to buy a strip center, the new loan on the apartment building would NOT be considered a purchase money loan, even though the proceeeds were used to buy a commercial property.

A purchase money commercial loan is a commercial loan that is used to buy a commercial property and which is secured by the same property. For example, if you refinanced your free-and-clear apartment building to buy a strip center, the new loan on the apartment building would NOT be considered a purchase money loan, even though the proceeeds were used to buy a commercial property.

Most purchase money commercial loans these days are SBA loans. If an established and profitable business wants to buy a larger facility, in order to expand and hire more workers, the SBA will guarantee a large portion of that loan. The buyer would only have to put down 10% of the purchase price (the new commercial loan would be 90% loan-to-value).

The opposite of an SBA loan is a conventional commercial mortgage loan. A conventional commercial mortgage loan is a commercial loan made with no government guarantee. By the way, the SBA is not the only Federal governmental agency that guarantees commercial loans. Don't forget that the USDA also guarantees commercial loans using its Business and Industry loan program. A USDA Business and Industry Loan is a commercial real estate loan, guaranteed by the USDA up to 90% LTV, and made in a rural, lowly-populated area, that will create more jobs in the rural area.

So a conventional commercial mortgage loan is a commercial mortgage loan that is not guaranteed by the SBA or the USDA. Most conventional commercial mortgage loans are made by either commercial banks or conduits. A commercial bank is just a garden variety bank, as opposed to an investment bank or a merchant bank. The word "commercial" is just a fancy word for "business" and signifies that the bank is in business to make a profit.

An investment bank is a company that sells stocks and bonds and occasionally takes companies public. A merchant bank is usually a small group of very wealthy investors - guys who often own a bank or life insurance company together - who use their excess profits to make equity investments in risky, potentially high-yielding investments. There are probably fewer than 200 merchant banking companies in the whole country, and you'll probably never get to meet one. If you ever meet a so-called "merchant banker" at some commercial lending conference, the chances are 20:1 that he is a con man, an advance fee scammer, and/or a huge slinger of bull-pucky. Mortals like you and me don't get to meet real merchant bankers.

Purchase money commercial loans are often used to buy commercial investment properties. Examples of commercial investment properties include apartment buildings, office buildings, shopping centers, strip centers, mobile home parks, and self storage facilities. They are properties where the income comes - not from running a business, like a restaurant or a bowling alley - but rather from plain-vanilla monthly rent. Commercial investment properties are purchased by real estate investors, rather than business owners.

Now we are finally getting to the point of this article. If a real estate investor wants to purchase a commercial investment property, like a multi-tenant office building, right now, the typical bank is going to require a huge downpayment. Why? Because commercial banks are too scared to lend higher than 58% to 62% loan-to-value on commercial investment properties.

To make matters worse, commercial banks will not let the seller carry back a second mortgage. Why? They don't want to over-burden the property with debt. They are afraid that if a tenant or two moves out and the cash flow dwindles, the commercial property owner might be tempted to use the cash flow earmarked for repairs and maintenance to make the payments on the second mortgage. Soon the property becomes dilapidated.

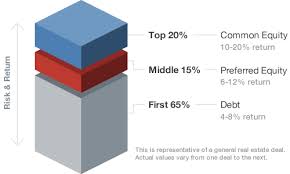

This means that buyers of commercial investment properties today have to put between 38% to 42% down in cash! Who has this kind of cash?

Now if the purchase price is huge, say $15 million or higher, the buyer will probably use a conduit loan (aka: CMBS loan). Behind the conduit loan, the buyer will often take out a mezzanine loan of $3 million to $5 million. Then the buyer will put just 25% down in cash. The mezzanine loan fills the gap in the capital stack between 65% LTV (the maximum exposure of a CMBS loan) and 75% loan-to-value.

A mezzanine loan is not a second mortgage. Instead, its a personal property loan against the membership interests of the LLC that owns one of these big, trophy commercial properties. Remember, a share of stock is personal property, not real property. A membership interest in an LLC is also personal property, not real property. Seizures (foreclosures) of personal property can be completed in less than six weeks. Real estate foreclosures can take 18 to 24 months in New York and many other states. This why these junior lenders make mezzanine loans, rather than second mortgages.

Therefore, if your investor is buying some huge, trophy commercial investment property for more than $15 million, he can probably get away with putting down as little as 25% of the purchase price, by using a CMBS loan, capped off by a mezzanine loan.

Unfortunately, mezzanine loans are legally very complicated. The legal fees alone can exceed $60,0000. As a result, few mezzanine lenders will make mezzanine loans of less $5 million (maybe $3 million).

Therefore, if a buyer of a commercial investment property is paying less $10 million to $15 million, he has a real problem. A commercial banks will only lend up to 58% to 62% LTV. This means he has to put down 38% to 42% of the purchase price. Not surprisingly, few smaller commercial investment properties are changing hands.

Until now.

Blackburne & Sons has just come out with an earth-shattering new commercial capital program. Our hard money mortgage company is now making Preferred Equity "Loans" from $100,000 to $600,000 nationwide.

Preferred Equity is actually not a loan. It's an equity investment. Legally we become part owners of the property; but we are only entitled to a Preferred Return that looks almost identical to garden-variety interest. Banks will allow Preferred Equity in "second position" because our payments are NOT required. If the property doesn't generate enough cash flow some month to make the Preferred Equity payments, the payments do NOT have to be made.

Don't worry about it if you are largely lost. At the end of this article, I'm going to give you a link to brand new white paper that explains Preferred Equity in layman's language.

Here's what you need to know: Commercial investment real estate is about to explode. There has been virtually no new commercial construction for six years. In the meantime, the U.S. has become the world's largest producer of oil. We have so much natural gas, and its so stinking cheap, that our heavy manufacturers have an enormous competitive advantage over every other country in the world. The U.S. economy - but for this miserable winter - should be exploding in production and hiring. It will happen this Spring.

Folks, I am the guy who warned you for a decade that a deflationary depression was coming. It came, but the Great Recession is over now. Commercial real estate is poised, after a 45% decline during the Great Recession, to march upwards for a decade.

Commercial real estate values are going to appreciate, and lots of investors are going to want to buy some. You won't be able to close any purchase money deals unless you find some company who can close the gap in the capital stack between 60% and 75%. This what our new Preferred Equity program does.

Folks, our new tiny Preferred Equity Program is the most important development in real estate finance since the second mortgage. You must - you absolutely MUST - download this free white paper and become more comfortable with Preferred Equity. It is the only way you will close purchase money commercial investment loans for the next five years.

A Special Use Property (aka: Single-Purpose Property) is a property whose design, construction, and use precludes uses other than that for which it was built.

A Special Use Property (aka: Single-Purpose Property) is a property whose design, construction, and use precludes uses other than that for which it was built.

If you have a balloon payment coming due on your commercial property, or if you are trying to buy an investment property, and you don't have a whopping 42% of the purchase price to put down in cash, this article is super-important to you.

If you have a balloon payment coming due on your commercial property, or if you are trying to buy an investment property, and you don't have a whopping 42% of the purchase price to put down in cash, this article is super-important to you. Commercial loans are still quite hard to close these days. Here are ten practical tips that will help you qualify for a commercial loan:

Commercial loans are still quite hard to close these days. Here are ten practical tips that will help you qualify for a commercial loan:

If you are a conventional buyer of commercial real estate, or if you are a commercial broker, this article is VERY important to you. The reason is because you are about to discover a BIG problem with your next commercial real estate loan.

If you are a conventional buyer of commercial real estate, or if you are a commercial broker, this article is VERY important to you. The reason is because you are about to discover a BIG problem with your next commercial real estate loan. Nobody is applying for commercial loans right now. In my 33 years in the commercial loan business, I have seldom seen the commercial real estate finance industry so dead.

Nobody is applying for commercial loans right now. In my 33 years in the commercial loan business, I have seldom seen the commercial real estate finance industry so dead.

Obtaining a commercial real estate loan these days is VERY expensive. There are lender points. There are broker points. There is an appraisal of the property by a General Certified Appraiser or an MAI appraiser. There is the toxic report. There is the survey and the title commitment. Some commercial lenders want an engineering report, and some even require a maximum probable loss (earthquake) report. There are also closing costs, like attorney's fees, escrow costs, and title insurance. The last thing a commercial property owner wants to do is to pay these fees and costs all over again when he gets a new commercial loan.

Obtaining a commercial real estate loan these days is VERY expensive. There are lender points. There are broker points. There is an appraisal of the property by a General Certified Appraiser or an MAI appraiser. There is the toxic report. There is the survey and the title commitment. Some commercial lenders want an engineering report, and some even require a maximum probable loss (earthquake) report. There are also closing costs, like attorney's fees, escrow costs, and title insurance. The last thing a commercial property owner wants to do is to pay these fees and costs all over again when he gets a new commercial loan.

Incoming commercial loan leads were outright crumby for

Incoming commercial loan leads were outright crumby for

Because we have been in the commercial mortgage loan business for over 33 years, and because we own CommercialMortgage.com, Blackburne & Sons just got approved to originate and sell apartment loans to this investor. These apartment loans actually close in our name, but they are quickly sold off to our institutional investor. The vetting process took over six months to complete, but we are now one of only six mortgage banking firms in the entire country allowed to originate loans for this investor in our own name.

Because we have been in the commercial mortgage loan business for over 33 years, and because we own CommercialMortgage.com, Blackburne & Sons just got approved to originate and sell apartment loans to this investor. These apartment loans actually close in our name, but they are quickly sold off to our institutional investor. The vetting process took over six months to complete, but we are now one of only six mortgage banking firms in the entire country allowed to originate loans for this investor in our own name. This may be one of my most important commercial loans blog articles ever because I explain almost a dozen new commercial finance

This may be one of my most important commercial loans blog articles ever because I explain almost a dozen new commercial finance