Are you building a small apartment building, office building, or flagged hotel? Is the bank demanding that you contribute an insane amount of equity to your deal? We may be able to help.

Are you building a small apartment building, office building, or flagged hotel? Is the bank demanding that you contribute an insane amount of equity to your deal? We may be able to help.

Blackburne & Sons Realty Capital Corporation can raise relatively small amounts of equity for new construction deals. We are looking to invest in fairly standard property types - the four major food groups (multifamily, office, retail, and industrial), plus self-storage and hospitality.

Sorry, but we will NOT consider residential development projects at this time. It is too late in the economic cycle. Homes will be slow to sell during a recession.

Example:

Davey Developer wants to develop a small apartment building in Indianapolis. The total cost is $10 million. Davey has contributed $2 million to the project, and normally that would be enough. Two million dollars is 20% of the total cost of the project. Historically banks have been happy to make construction loans of 80% loan-to-cost.

But when Davey Developer sits down with Louie the Loan Officer for Nearby Bank*, Louie says, "I'm sorry, Davey, you've been a great customer of the bank for years. Your two deals, for which we provided the construction loan, went off without a hitch. Your new buildings were gorgeous, and the quality was obvious."

"However, like a great many banks, Nearby Bank got seriously hurt in construction lending during the Great Recession. In fact, Davey, we almost went under. Yikes. As a result of pressure from regulators, we can now only make construction loans if the developer contributes 35% of the total cost of the project. Every other bank in Central Indiana is subject to the same bank regulations, so it will do you little good to try to find another bank."

"In this case," continues Louie the Loan Officer, "the total cost of your project is $10 million. You'll need a total of $3,500,000 in equity. You only have $2 million to contribute to the project, so you'll need to somehow raise another $1,500,000."

*For training purposes, I have used the name of Nearby Bank for the construction lender. Remember, commercial construction loans are almost always made by commercial banks, and the closer the bank is located to the proposed project, the more likely it is that the bank will approve the deal.

Davey's deal is just what Blackburne & Sons is seeking. The fact that he has built two prior projects shows that he has experience, and the need for $1.5 million in additional equity is right in our sweet spot.

Our sweet spot is to contribute up to $2 million in equity. Raising equity is a lot harder than raising hard money loan dollars because the investment is immensely riskier. An equity investor can easily lose 100% of his dough if the construction lender forecloses.

On the other hand, equity investors have a chance to earn much higher yields, on the order of 18% to 30% annualized return on their investment (ROI).

Think about this from a developer's point of view. The bank will loan him capital at just 6.5% interest, but an equity investor will want a 18% to 30% ROI. Obviously, the developer will want as many loan dollars as the bank is willing to give him.

Mortgage brokers, if you are trying to place a construction loan, and the developer is short a little equity, you should bring in Blackburne & Sons to provide the last piece of equity.

We are not going to provide 100% of the equity in a commercial construction deal. We want the developer to have a ton of his own skin in the game. We certainly don't want him walking away. As a result, we will not contribute more than 40% of the required equity.

Got a deal? Please do NOT call me. Please do NOT send me a package. I probably won't even look at it (too long). Instead, please just send me, George Blackburne III (the old man and father of George IV) a ONE paragraph pitch that mirrors the following:

Sample Equity Contribution Request:

George,

I am building a spec office building in Billings, Montana, where nearby oil exploration has driven the office vacancy rate down to below 5% (give me a little sizzle here). The total cost of the project is $8 million, and my construction lender will only go 60% of cost. I need a total $3.2 million in equity, and I am short $1.3 million in equity.

Love,

Donny Developer (no relation to Davey)

Important Note:

I get 1,500 emails every single day, so it is critical that the subject line read exactly, "Equity Contribution Request"; otherwise, it will be too easy for me to miss your important email.

If your deal looks like a good fit, I'll ask for your package, and I'll send you my phone number. Thanks!

Are you a wealthy and accredited investor? Does the idea of earning 18% to 25% on your money sound attractive? Blackburne & Sons (est. 1980) started out as a hard money lender that recently expanded into syndication. Our accredited investors (about 2,000 of them) receive both first mortgage investment opportunities AND equity investment opportunities from us. If you fill out the form below, we'll add you to our investment distribution list. We are actually going out for sale on an equity deal that is projected to yield 25.4% to our investors, and the builder has built SIXTY hotels. Wow. Yum.

Today we are going to talk about

Today we are going to talk about

This article is more about economics than than commercial loan training. I hope that you investors will find it interesting.

This article is more about economics than than commercial loan training. I hope that you investors will find it interesting.

Before I get into the subject of placing a commercial loan with a bank, I have two great TV show recommendations.

Before I get into the subject of placing a commercial loan with a bank, I have two great TV show recommendations.

Every two-and-a-half years, I suck it up and write a check for thousands of dollars to my staff to update

Every two-and-a-half years, I suck it up and write a check for thousands of dollars to my staff to update

Any commercial loan broker with more than six-month's worth of experience will tell you, "Daisy chains never close." A

Any commercial loan broker with more than six-month's worth of experience will tell you, "Daisy chains never close." A

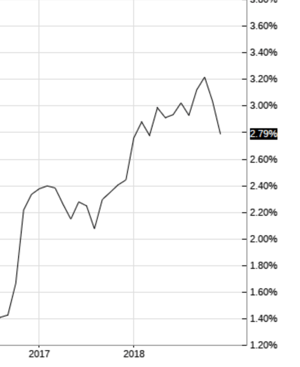

By the end of this training article, you will know what banks are quoting on commercial loans on office buildings, retail buildings, shopping centers, and industrial buildings; i.e., what commercial banks are quoting on permanent loans.

By the end of this training article, you will know what banks are quoting on commercial loans on office buildings, retail buildings, shopping centers, and industrial buildings; i.e., what commercial banks are quoting on permanent loans.

Whenever a commercial mortgage lender offers you or your client an adjustable mortgage loan (AML), it is very important that you compute the implied rate before accepting the loan.

Whenever a commercial mortgage lender offers you or your client an adjustable mortgage loan (AML), it is very important that you compute the implied rate before accepting the loan.

Swap spreads is another popular index in commercial real estate finance.

Swap spreads is another popular index in commercial real estate finance.

I have no lessons about commercial loans today. Instead, let's just have some fun on this relaxing Boxing Day.

I have no lessons about commercial loans today. Instead, let's just have some fun on this relaxing Boxing Day.

So I told you that we have a dog door for our animals to go out, but wild animals can come in using that door. We first realized that we had a problem when we discovered that local raccoons were carefully washing their paws in our water bowl before dining on our dog food. "For these gifts we are about to receive..." Then the HUGE neighborhood tom cat got trapped by our dogs in our house. That darned cat was so big and fierce that he had absolutely no fear of me. I found myself backing up. Buck-buck-buck. Haha!

So I told you that we have a dog door for our animals to go out, but wild animals can come in using that door. We first realized that we had a problem when we discovered that local raccoons were carefully washing their paws in our water bowl before dining on our dog food. "For these gifts we are about to receive..." Then the HUGE neighborhood tom cat got trapped by our dogs in our house. That darned cat was so big and fierce that he had absolutely no fear of me. I found myself backing up. Buck-buck-buck. Haha!