This article should be particularly interesting to accredited investors, commercial brokers (realtors), and commercial mortgage brokers because it describes a way for you to find the Holy Grail of real estate - equity money.

This article should be particularly interesting to accredited investors, commercial brokers (realtors), and commercial mortgage brokers because it describes a way for you to find the Holy Grail of real estate - equity money.

It is sometimes hard to fathom a world where such financial industry giants, as Lehman Brothers, Home Savings of America (once the largest S&L in the country), EF Hutton, Paine Webber, and Countrywide Financial, have now all either gone bankrupt or have been absorbed by a larger company into non-relevance.

When I was new to the mortgage business, Home Savings was like the Roman Empire. Their enormous branch offices - each an architectural landmark like the Parthenon - were everywhere. They're gone now?

Billions were spent just marketing the names of these companies. "When EF Hutton speaks, people listen." Every day for for decades, and during every pro football game, you would hear their commercials. Now the name, EF Hutton, is just a distant memory.

There was another financial empire, a veritable colossus, that you may never have heard about - the syndication industry. Was it a big industry? Did they make a lot of money? Think hundreds of billions of dollars worth of investments. Think of an that was ten times larger than the entire hard money business. Think big mansions, fast cars, and expensive parties. Syndicators were at the top of the financial food chain.

But what is a syndicator? A syndicator is a broker-dealer who puts together groups of wealthy private investors, known as accredited investors, to buy and hold commercial real estate. But what is a broker-dealer?

A broker-dealer (think: stock broker) is a person or firm in the business of buying and selling securities, operating as both a broker and a dealer, depending on the transaction. The term broker-dealer is used in U.S. securities regulation parlance to describe stock brokerages, because most of them act as both agents and principals (investing with their own dough). A brokerage acts as a broker (or agent) when it executes orders on behalf of clients, whereas it acts as a dealer, or principal, when it trades for its own account.

Broker-dealers are heavily regulated by the NASD, the National Association of Securities Dealers. Hence their downfall. By the time the Syndication Crisis was over, on the order of 70% (90%?) of all broker-dealers were out of business (and some were facing jail time).

It all started in the late 1970's, before the Reagan Administration. Back in the day, the top tax rate was 90%! But this tax rate was deceiving. There were all sorts of tax shelters, where a taxpayer could lower his tax rate by investing his dough where the government wanted. One of these tax shelters was multifamily and commercial construction.

Under the tax code prior to 1986, a doctor would invest several hundred thousand dollars into a limited partnership, put together by a syndicator, which would buy an apartment building using leverage; i.e., some bank would finance 70% of the purchase.

This leveraged investment would intentionally produce a paper loss every year, largely due to depreciation. The early limited partnerships were properly structured. The early syndicators used just the right amount of equity (dough from the doctors). While there was a paper loss, there was no actual out-of-pocket loss, called an alligator, for the investors.

A typical doctor would then take his $50,000 paper loss and use it to reduce his taxable income from $400,000 per year to just $350,000 per year. Since the top tax rate was 90%, the doctor saved 90% of that $50,000 reduction in taxable income. All was good in the world because the Federal government was trying to encourage the construction of new apartment buildings.

And the syndicators got rich, rich, rich.

But like most manias, things got out of hand. Eventually so many apartment buildings were constructed that they became over-built in some areas. To make matter worse, syndicators began to structure deals with super-sized losses. Syndicators would assemble syndicates with so little equity (doctor money) and with so much debt that the deals intentionally had a negative cash flow. Yikes.

These 1984 and 1985-era syndicates had large negative cash flows that had to be fed by assessing the doctors every month to feed the alligator. When the general partner of a limited partnership - or modernly the Managing Member of a limited liability company - has to ask the investors for more cash, it is called a cash call. Back in 1984 and 1985, the doctors didn't mind monthly cash calls because the negative cash flows produced super-sized tax shelter losses.

"Would you like me to super-size your alligator?" Ha-ha!

When President Reagan was elected, he led a charge to change the U.S. tax code. Tax shelter investments were no longer going to where they would produce the best benefit for the economy, but rather they were going into real estate deals where the real estate was hardly needed.

The Tax Reform Act of 1986 radically changed the commercial property market. No longer could wealthy investors shelter their active income from employment with passive losses from real estate. Suddenly one of the legs propping up commercial real estate values was kicked out from the under the industry. "If I can't use the building as a tax shelter, then dump the dang thing! I want out."

Commercial real estate values then plunged by 45%. Remember that number - 45%. When commercial real estate crashes, it falls exactly 45% and not a penny more. I have seen commercial real estate crash exactly 45% three times in my career - the S&L Crisis (includes this tax change), the Dot Com Crisis, and the Great Recession. Remember this during the next crisis, when the Chicken Little's of this world are shouting that the sky is falling. The time to buy is when blood is running in the streets, when commercial real estate has fallen 45%.

But the General Partner of the limited partnerships, the broker-dealer that syndicated the deal, couldn't sell the property. After a 45% decline in commercial real estate values, the partnership owed far more on the property than it was worth.

And thing got worse. Under the old limited partnerships, the general partner was personally liable for the debt. Holy crapola! Guess who was the general partner? The syndicator, the broker-dealer who assembled the syndicate.

"But wait, weren't the doctors still liable for their cash calls?" Maybe in theory, but in real life they all told the syndicators to go pound sand. The banks foreclosed and obtained huge deficiency judgments against the general partners. Facing countless collection actions from banks, the broker-dealers then filed for bankruptcy, one after the other.

When Europeans landed in the New World, they brought the small box virus. There were 25 million Native-Americans in North America. About 21 million of them died of smallpox or other European diseases, for which they had no immunity. Bankruptcies swept through the broker-deal industry in the late 1980's and early 1990's, just like a smallpox epidemic. Virtually every small broker-dealer in the country was wiped out.

The syndication industry was suddenly gone - poof! An industry involving hundreds of billions of dollars simply disappeared. And it never came back.

Blackburne & Sons Realty Capital Corporation is returning to the syndication business. We have already closed a dozen small deals, and we made an offer on another Sacramento purchase this week. Unfortunately we are focusing strictly on the Sacramento area right now, so we are not quite ready to ask for deals.

The deals we are doing are 100% all-cash deals. Our deals are capital preservation deals, where there is zero debt. The idea is to create a "partnership" (more precisely a new LLC) that can withstand just about any financial crisis.

Participation right now is being limited to our trust deed investors and those accredited investors who have signed up for our trust deed distribution list. The best way to start seeing these deals - assuming you are an accredited investor - is to sign up for on trust deed distribution list.

Dan Harkey has worked for over 45 years in the hard money lending business. (To old veterans like myself, Dan is respected as an icon.). He currently consults with borrowers in need of hard money loans. Dan can be reached at 949-533-8315 or at dan@danharkey.com.

Dan Harkey has worked for over 45 years in the hard money lending business. (To old veterans like myself, Dan is respected as an icon.). He currently consults with borrowers in need of hard money loans. Dan can be reached at 949-533-8315 or at dan@danharkey.com.

All of my work life I have heard smart real estate people use fancy terms like conforming, legal nonconforming, illegal nonconforming, conditional use permits, and variances. I would always nod my head and try to look intelligent, but the truth is that I never knew what the heck they were talking about.

All of my work life I have heard smart real estate people use fancy terms like conforming, legal nonconforming, illegal nonconforming, conditional use permits, and variances. I would always nod my head and try to look intelligent, but the truth is that I never knew what the heck they were talking about.

Dan Harkey has worked for over 45 years in the hard money lending business. (To old veterans like myself, Dan is respected as an icon.). He currently consults with borrowers in need of hard money loans. Dan can be reached at 949-533-8315 or at dan@danharkey.com.

Dan Harkey has worked for over 45 years in the hard money lending business. (To old veterans like myself, Dan is respected as an icon.). He currently consults with borrowers in need of hard money loans. Dan can be reached at 949-533-8315 or at dan@danharkey.com. What on earth is a TIC roll-up? Do they bite when you try to roll them up?

What on earth is a TIC roll-up? Do they bite when you try to roll them up?

I have a real treat for you today. A buddy of mine, Yoni Miller of

I have a real treat for you today. A buddy of mine, Yoni Miller of

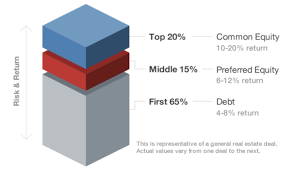

QuickLiquidity is a direct lender and preferred equity investor providing equity recapitalizations, subordinated debt and partner buyouts on commercial real estate nationwide. QuickLiquidity allows real estate owners to monetize their existing equity while maintaining majority ownership and control of their property without disturbing their existing first mortgage or triggering any prepayment penalties. For more information you can visit www.quickliquidity.com/recapitalizations.html or call Yoni Miller 561-221-0881.

QuickLiquidity is a direct lender and preferred equity investor providing equity recapitalizations, subordinated debt and partner buyouts on commercial real estate nationwide. QuickLiquidity allows real estate owners to monetize their existing equity while maintaining majority ownership and control of their property without disturbing their existing first mortgage or triggering any prepayment penalties. For more information you can visit www.quickliquidity.com/recapitalizations.html or call Yoni Miller 561-221-0881.

If you are a multifamily or commercial property investor yourself, today's training article is really going to open your eyes. Banks dislike you just for breathing.

If you are a multifamily or commercial property investor yourself, today's training article is really going to open your eyes. Banks dislike you just for breathing.

Whether you're a borrower, commercial broker, or commercial loan broker, today's super quick lesson applies to you.

Whether you're a borrower, commercial broker, or commercial loan broker, today's super quick lesson applies to you.

When applying for a commercial loan to buy a small apartment building

When applying for a commercial loan to buy a small apartment building

Commercial loan brokers and borrowers often give up far too easily. They get a commercial loan application in the door that they think is pretty good. Then they take the deal to three or four commercial banks, who proceed to criticize the deal to death. "I don't like the location." "The borrower isn't strong enough." "One of the leases expires in just 14 months." "The borrower doesn't have enough liquidity."

Commercial loan brokers and borrowers often give up far too easily. They get a commercial loan application in the door that they think is pretty good. Then they take the deal to three or four commercial banks, who proceed to criticize the deal to death. "I don't like the location." "The borrower isn't strong enough." "One of the leases expires in just 14 months." "The borrower doesn't have enough liquidity."